Unlocking the Next Wave of Precision: How GNSS Augmentation is Transforming Positioning Services Worldwide

- Market Overview: The Expanding Role of Precision Positioning

- Technology Trends: Innovations in GNSS Augmentation and Positioning

- Competitive Landscape: Key Players and Strategic Moves

- Growth Forecasts: Projected Expansion of Precision Services

- Regional Analysis: Hotspots and Emerging Markets

- Future Outlook: The Road Ahead for GNSS-Enabled Precision

- Challenges & Opportunities: Navigating Barriers and Unlocking Potential

- Sources & References

“Tech News Deep Dive: July 2025 Microsoft’s Massive Restructuring: Layoffs, AI Investments, and Gaming Turmoil Microsoft is making headlines with a sweeping round of layoffs, cutting approximately 9,000 jobs—about 4% of its global workforce.” (source)

Market Overview: The Expanding Role of Precision Positioning

The global market for precision positioning services, driven by advancements in Global Navigation Satellite System (GNSS) augmentation, is experiencing rapid expansion. As industries such as agriculture, construction, autonomous vehicles, and geospatial surveying increasingly demand centimeter-level accuracy, the value of GNSS augmentation and positioning services is projected to double by 2030.

According to a recent report by the European GNSS Agency (GSA), the global GNSS market is expected to reach €325 billion by 2029, with high-precision applications representing one of the fastest-growing segments. The proliferation of Real-Time Kinematic (RTK), Precise Point Positioning (PPP), and network-based augmentation services is enabling sub-meter to centimeter-level accuracy, unlocking new use cases and revenue streams.

- Agriculture: Precision farming is leveraging GNSS augmentation for automated guidance, variable rate application, and field mapping. The adoption of these technologies is forecast to increase the global precision agriculture market to $15.6 billion by 2030 (MarketsandMarkets).

- Autonomous Vehicles: The need for lane-level accuracy in autonomous driving is fueling demand for high-precision GNSS services. The global autonomous vehicle market is projected to reach $2.3 trillion by 2030, with positioning services forming a critical component (Statista).

- Construction & Surveying: GNSS-based machine control and surveying solutions are streamlining workflows and reducing costs. The construction industry’s adoption of these technologies is expected to contribute significantly to the doubling of the market size (GPS World).

Major players such as Trimble, Hexagon, and Topcon are expanding their service offerings, while new entrants and regional providers are increasing competition and innovation. The rollout of next-generation GNSS constellations (e.g., Galileo, BeiDou) and the integration of IoT and 5G are further enhancing the reliability and accessibility of precision positioning services.

In summary, the “precision gold rush” is underway, with GNSS augmentation and positioning services poised to double in market value by 2030, reshaping industries and enabling a new era of location-based innovation.

Technology Trends: Innovations in GNSS Augmentation and Positioning

The global market for GNSS (Global Navigation Satellite System) augmentation and high-precision positioning services is experiencing a rapid expansion, driven by surging demand across sectors such as agriculture, construction, autonomous vehicles, and geospatial surveying. According to a recent report by the European GNSS Agency (GSA), the worldwide GNSS market is projected to reach €325 billion by 2029, with high-precision applications representing one of the fastest-growing segments.

Key innovations fueling this growth include:

- Real-Time Kinematic (RTK) and Precise Point Positioning (PPP): These technologies enable centimeter-level accuracy, essential for applications like precision agriculture and autonomous navigation. The adoption of network RTK and PPP-RTK services is expanding, with providers such as Trimble and Topcon rolling out global correction networks.

- Multi-constellation and Multi-frequency Receivers: Modern GNSS receivers now leverage signals from GPS, Galileo, GLONASS, and BeiDou, improving reliability and accuracy even in challenging environments. This trend is accelerating as more satellites are launched and new frequencies become available (GPS World).

- Cloud-based and IoT Integration: The integration of GNSS data with cloud platforms and IoT devices is enabling real-time analytics and remote monitoring, particularly in fleet management and smart city infrastructure (MarketsandMarkets).

Market forecasts indicate that the global high-precision GNSS services market will more than double by 2030, reaching an estimated $10 billion, up from $4.2 billion in 2022 (GlobeNewswire). This surge is attributed to:

- Widespread adoption of autonomous and semi-autonomous systems in agriculture and construction

- Expansion of smart transportation and logistics solutions

- Growing demand for accurate geospatial data in urban planning and environmental monitoring

As GNSS augmentation technologies continue to evolve, the “precision gold rush” is set to transform industries, enabling new business models and unlocking unprecedented value from location-based services worldwide.

Competitive Landscape: Key Players and Strategic Moves

The global market for GNSS (Global Navigation Satellite System) augmentation and positioning services is experiencing a rapid transformation, driven by the surging demand for high-precision location data across industries such as agriculture, construction, autonomous vehicles, and geospatial services. According to a recent report by GlobeNewswire, the GNSS market is projected to more than double by 2030, reaching a value of over $400 billion, up from approximately $200 billion in 2022. This growth is fueled by the proliferation of IoT devices, smart infrastructure, and the increasing adoption of real-time kinematic (RTK) and precise point positioning (PPP) technologies.

Key Players and Strategic Moves

- Trimble Inc. – A global leader in GNSS solutions, Trimble continues to expand its portfolio through acquisitions and partnerships. In 2023, Trimble announced the integration of its RTX correction services with major agricultural machinery brands, enhancing precision farming capabilities (Trimble Agriculture).

- Hexagon AB – Through its subsidiary Leica Geosystems, Hexagon has invested heavily in cloud-based GNSS augmentation networks. The company’s HxGN SmartNet is now one of the world’s largest reference station networks, supporting applications from surveying to autonomous vehicles (HxGN SmartNet).

- Topcon Positioning Systems – Topcon is focusing on integrated solutions for construction and agriculture, leveraging its Topnet Live GNSS correction service to deliver centimeter-level accuracy globally (Topcon GNSS Solutions).

- Septentrio – Known for its robust GNSS receivers, Septentrio is targeting industrial automation and robotics, recently launching new modules optimized for resilience against interference and spoofing (Septentrio GNSS Receivers).

- u-blox – Specializing in scalable GNSS modules, u-blox is expanding its reach in automotive and IoT, with recent partnerships to deliver high-precision positioning for connected vehicles (u-blox GNSS Modules).

Strategically, these players are investing in cloud-based correction services, expanding reference station networks, and forming cross-industry alliances to address the growing need for reliable, real-time, and high-accuracy positioning. As the “precision gold rush” accelerates, the competitive landscape is expected to intensify, with innovation and scalability as key differentiators.

Growth Forecasts: Projected Expansion of Precision Services

The global market for GNSS (Global Navigation Satellite System) augmentation and high-precision positioning services is entering a period of rapid expansion, often described as a “precision gold rush.” Driven by surging demand in sectors such as agriculture, construction, autonomous vehicles, and geospatial surveying, the market is projected to more than double in value by 2030.

According to a recent report by the European GNSS Agency (GSA), the global GNSS market is expected to reach €510 billion (approximately $550 billion) by 2032, with high-precision applications representing one of the fastest-growing segments. The high-precision GNSS market, which includes Real-Time Kinematic (RTK), Precise Point Positioning (PPP), and augmentation services, is forecasted to grow at a CAGR of over 15% through 2030 (MarketsandMarkets).

Key drivers of this growth include:

- Autonomous Systems: The proliferation of autonomous vehicles, drones, and robotics is fueling demand for centimeter-level accuracy, which only GNSS augmentation can provide.

- Smart Agriculture: Precision farming techniques, reliant on GNSS-based guidance and mapping, are expected to see adoption rates climb, especially in North America, Europe, and Asia-Pacific (GlobeNewswire).

- Construction & Surveying: Digital construction and geospatial data collection are increasingly dependent on high-accuracy positioning, driving service uptake.

- Infrastructure Expansion: The rollout of new GNSS constellations and regional augmentation systems (e.g., EGNOS, WAAS, BeiDou) is enhancing global coverage and reliability.

By 2030, the number of devices using high-precision GNSS services is expected to exceed 1 billion, up from around 300 million in 2022 (GSA Market Report). This surge is attracting significant investment from both established players and new entrants, intensifying competition and accelerating innovation in service delivery and pricing models.

In summary, the precision GNSS augmentation and positioning services sector is on track for exponential growth, underpinned by technological advances and expanding application domains. Stakeholders across the value chain are poised to benefit from this “precision gold rush” as the market doubles in size by the end of the decade.

Regional Analysis: Hotspots and Emerging Markets

The global market for GNSS (Global Navigation Satellite System) augmentation and positioning services is experiencing a significant surge, with industry analysts projecting the market to double in value by 2030. This growth is fueled by the increasing demand for high-precision location data across sectors such as agriculture, construction, autonomous vehicles, and geospatial surveying. According to a recent report by the European GNSS Agency (GSA), the worldwide GNSS market is expected to reach €325 billion by 2029, with augmentation services representing a rapidly expanding segment.

Regional Hotspots

- Asia-Pacific: The Asia-Pacific region is emerging as a dominant force, driven by large-scale infrastructure projects and government-backed initiatives in China, Japan, South Korea, and India. China’s BeiDou system and India’s NavIC are spurring domestic innovation and adoption, with the Asia-Pacific GNSS market forecasted to grow at a CAGR of over 10% through 2030 (GlobeNewswire).

- North America: The United States and Canada continue to lead in precision agriculture and autonomous vehicle development, leveraging GPS and commercial augmentation networks. The U.S. market is bolstered by investments in real-time kinematic (RTK) and precise point positioning (PPP) services, with North America accounting for nearly 35% of global GNSS revenues (MarketsandMarkets).

- Europe: The European Union’s Galileo system and EGNOS augmentation are central to the region’s strategy, supporting smart mobility and logistics. The EU is investing in resilient, high-accuracy services for critical infrastructure and urban mobility, with the region’s GNSS market expected to reach €100 billion by 2030 (GSA).

Emerging Markets

- Latin America and Africa: These regions are witnessing rapid adoption of GNSS augmentation in agriculture, mining, and land management. Brazil and South Africa are leading the charge, with public-private partnerships expanding access to high-precision services (GPS World).

- Middle East: Investments in smart cities and logistics hubs, particularly in the UAE and Saudi Arabia, are driving demand for advanced positioning solutions.

As GNSS augmentation and positioning services become integral to digital transformation, regional hotspots and emerging markets are poised to capture significant value, making this a true “precision gold rush” through 2030.

Future Outlook: The Road Ahead for GNSS-Enabled Precision

The global market for GNSS (Global Navigation Satellite System) augmentation and high-precision positioning services is on the cusp of a significant expansion, often described as a “precision gold rush.” Driven by surging demand across sectors such as agriculture, construction, autonomous vehicles, and geospatial surveying, the market is projected to more than double in value by 2030.

According to a recent report by the European GNSS Agency (GSA), the worldwide GNSS market is expected to reach €510 billion by 2031, with high-precision applications representing one of the fastest-growing segments. The proliferation of real-time kinematic (RTK), precise point positioning (PPP), and network-based augmentation services is enabling centimeter-level accuracy, which is critical for next-generation applications.

- Agriculture: Precision farming is rapidly adopting GNSS augmentation to optimize planting, fertilization, and harvesting. The precision agriculture market is forecasted to grow from $8.5 billion in 2023 to $15.6 billion by 2030, with GNSS services as a core enabler.

- Autonomous Vehicles: Self-driving cars, drones, and robotics require reliable, high-precision positioning. The GNSS market for automotive and UAVs is expected to see double-digit CAGR through 2030.

- Construction & Surveying: Digital construction and smart infrastructure rely on GNSS for site layout, machine control, and asset management. The GNSS-enabled construction market is projected to expand rapidly as digital transformation accelerates.

Key players such as Trimble, Hexagon, Topcon, and u-blox are investing heavily in cloud-based correction services, multi-constellation support, and integration with IoT platforms. Meanwhile, government initiatives like the European Galileo High Accuracy Service (HAS) and China’s BeiDou augmentation are democratizing access to high-precision signals (Inside GNSS).

As GNSS augmentation becomes more accessible and affordable, the precision gold rush is set to transform industries, unlock new business models, and drive the market to unprecedented heights by 2030.

Challenges & Opportunities: Navigating Barriers and Unlocking Potential

The global market for GNSS (Global Navigation Satellite System) augmentation and high-precision positioning services is experiencing a transformative surge, often dubbed the “Precision Gold Rush.” As industries such as agriculture, construction, autonomous vehicles, and geospatial services increasingly demand centimeter-level accuracy, the market is projected to more than double by 2030. According to a recent report by European GNSS Agency (GSA), the global GNSS market is expected to reach €325 billion by 2029, with high-precision applications representing one of the fastest-growing segments.

Challenges

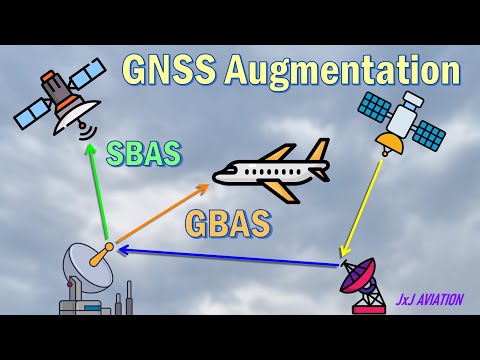

- Infrastructure Investment: The deployment of ground-based augmentation systems (GBAS), real-time kinematic (RTK) networks, and precise point positioning (PPP) services requires significant capital expenditure. Many regions, especially in developing economies, face hurdles in justifying and funding such investments.

- Interoperability & Standardization: The proliferation of proprietary solutions and lack of universal standards complicate integration across platforms and industries. This fragmentation can slow adoption and limit the scalability of services (GPS World).

- Cybersecurity & Signal Integrity: As reliance on GNSS grows, so does vulnerability to spoofing, jamming, and cyberattacks. Ensuring signal integrity and resilience is a critical technical and regulatory challenge.

- Regulatory Hurdles: Varying national regulations regarding spectrum allocation, data privacy, and liability can impede cross-border service provision and slow market expansion.

Opportunities

- Autonomous Systems: The rapid development of autonomous vehicles, drones, and robotics is driving demand for ultra-precise positioning. The automotive sector alone is expected to account for a significant share of the market’s growth (MarketsandMarkets).

- Smart Agriculture: Precision farming, enabled by GNSS augmentation, can increase crop yields by up to 20% while reducing input costs, presenting a compelling value proposition for agribusinesses worldwide (Statista).

- Emerging Markets: Asia-Pacific and Latin America are poised for rapid adoption as infrastructure investments accelerate and regulatory frameworks mature.

- Integration with IoT & 5G: The convergence of GNSS with IoT devices and 5G networks will unlock new applications in asset tracking, smart cities, and logistics, further expanding the addressable market.

In summary, while the path to doubling the GNSS augmentation and positioning services market by 2030 is marked by significant challenges, the opportunities for innovation, efficiency, and new business models are equally compelling. Stakeholders who can navigate regulatory, technical, and investment barriers stand to benefit most from this precision-driven gold rush.

Sources & References

- Precision Gold Rush: GNSS Augmentation & Positioning Services Set to Double by 2030

- European GNSS Agency (GSA)

- MarketsandMarkets

- Statista

- GPS World

- Trimble Agriculture

- Topcon GNSS Solutions

- GNSS market for automotive and UAVs

- Septentrio GNSS Receivers

- u-blox GNSS Modules

- Inside GNSS